Injuries happen. Sometimes they occur at work, and sometimes they result from someone else’s carelessness. When you’re hurt, understanding your rights is crucial. Two common legal avenues for seeking compensation are workers’ compensation and personal injury claims. But what are the differences, and which one applies to your situation? Let’s break it down in plain language.

Understanding Workers’ Compensation: Your Rights and Benefits

Workers’ compensation is a type of insurance that provides benefits to employees who are injured or become ill as a direct result of their job. Think of it as a safety net designed to protect you if you get hurt while working.

Key features of workers’ compensation:

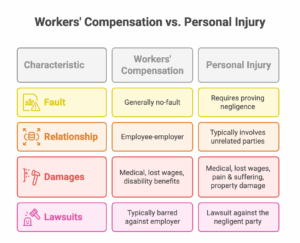

- No-Fault System: This is a big one. You generally don’t have to prove your employer was negligent to receive benefits. If you were injured while performing your job duties, you’re likely covered.

- Benefits Covered: Workers’ comp typically covers medical expenses, lost wages (usually a portion of your regular salary), and in some cases, permanent disability benefits.

- Filing a Claim: The process typically involves reporting the injury to your employer as soon as possible. They, in turn, should file a claim with their workers’ compensation insurance carrier. You’ll likely need to see a doctor authorised by the insurance company for evaluation and treatment.

- Employer Protection: In exchange for providing this “no-fault” coverage, employers are generally protected from lawsuits by their employees for work-related injuries. This is known as the “exclusive remedy” rule.

Example: Sarah, a warehouse worker, slipped and fell while stocking shelves. Even though her employer wasn’t directly at fault, she’s likely eligible for workers’ compensation to cover her medical bills and lost wages while she recovers.

Exploring Personal Injury Claims: Negligence and Liability

A personal injury claim arises when you’re injured due to someone else’s negligence – meaning they failed to exercise reasonable care, and that failure caused your injury. These claims can stem from various incidents, including car accidents and slip-and-fall accidents on someone else’s property.

Key features of personal injury claims:

- Negligence Required: Unlike workers’ comp, you must prove that the other party was negligent. This involves demonstrating that they had a duty of care, breached that duty, their breach caused your injury, and you suffered damages as a result.

- Types of Damages: Personal injury claims can cover a broader range of damages than workers’ comp, including medical expenses, lost wages, property damage, pain and suffering, and emotional distress.

- Comparative Negligence: Your negligence can impact your recovery. Many states follow “comparative negligence” rules, where the percentage of your fault reduces your compensation. For example, if you’re deemed 20% responsible for a car accident, you might only recover 80% of your damages.

Example: John was hit by a driver who ran a red light. He suffered injuries and damage to his car. John can file a personal injury claim against the at-fault driver to recover his medical bills, lost wages, car repair costs, and compensation for his pain and suffering.

Dealing with Uninsured/Underinsured Drivers: What happens if the at-fault driver doesn’t have insurance or enough insurance to cover your damages? This is where uninsured/underinsured motorist coverage in your auto policy comes into play. It provides a safety net when the responsible party can’t fully compensate you.

Handling Property Damage: Separately from the injury claim, you’ll also need to address property damage to your vehicle. This often involves dealing directly with the at-fault driver’s insurance or, in the case of an uninsured driver, your collision coverage. Get multiple estimates for repairs to ensure fair compensation.

Key Differences Between Workers’ Compensation and Personal Injury Cases

When Can a Personal Injury Claim Arise from a Work-Related Accident?

While the “exclusive remedy” rule usually prevents you from suing your employer for a work injury, there are exceptions. A personal injury claim might be possible in addition to workers’ compensation if a third party was responsible for your injury at work.

Examples:

- Defective Equipment: If you’re injured at work by a faulty machine manufactured by a third-party company, you might be able to file a personal injury claim against that company.

- Car Accident on a Work Errand: Let’s say you’re driving for work and are hit by another driver. You could file a workers’ compensation claim and a personal injury claim against the at-fault driver.

- Negligence of Another Contractor: If another company’s employee on your worksite acts negligently, causing your injury, you may have grounds for a personal injury claim against the other company.

Pursuing Both Workers’ Compensation and a Personal Injury Claim: Is it Possible?

Yes, it is sometimes possible to pursue both workers’ compensation and a personal injury claim, but it’s crucial to understand how they interact. Workers’ compensation often acts as a primary payer for medical bills and lost wages. Any settlement or judgment from a personal injury case might be subject to a lien by the workers’ compensation insurer to recoup benefits they’ve already paid. This is to prevent you from receiving a double recovery for the same damages.

Example: Let’s revisit John, who was hit by a negligent driver while on a work errand. He receives workers’ compensation benefits for his medical bills and lost wages. He also wins a personal injury settlement against the at-fault driver. The workers’ compensation insurer likely has a right to be reimbursed from the personal injury settlement for the benefits they already paid to John.

Seeking Legal Guidance: Getting the Right Help

Workers’ compensation and personal injury laws can be comple and intricatex. It’s smart to seek guidance from an experienced attorney. A lawyer can assess your specific situation, explain your rights, and help you navigate the claims process. They can help determine if you have a valid personal injury claim in addition to workers’ compensation, maximise your potential recovery, and protect your interests. Don’t leave money on the table – get the help you deserve!